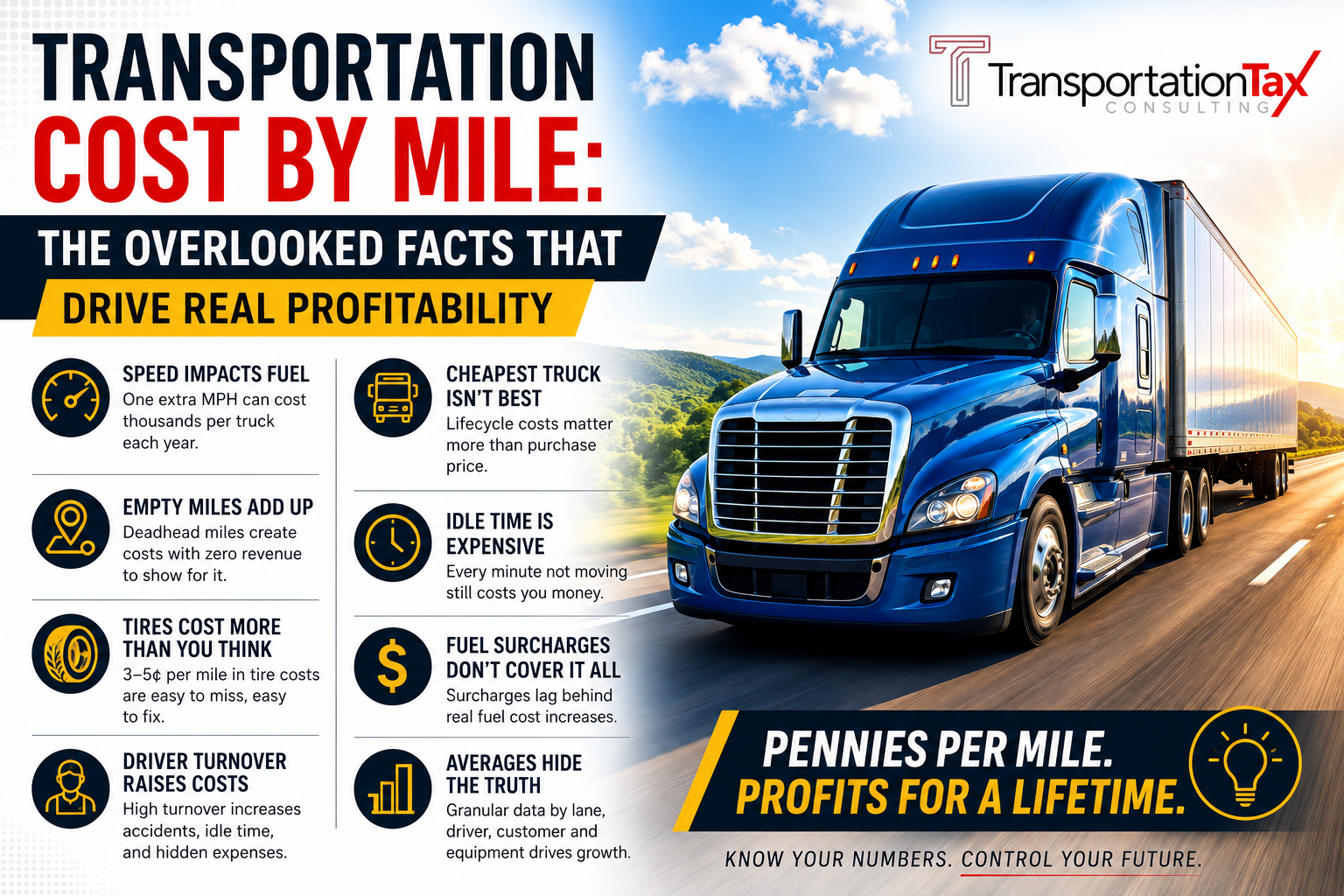

Truck Tariffs Begin Nov. 1: What You Need to Know

Share this Article:

Beginning Nov. 1, 2025, the U.S. will impose a 25% tariff on imported medium- and heavy-duty trucks (Classes 3 through 8), according to a recent announcement by the Trump administration. While this move is intended to protect domestic manufacturers, it carries broad implications for transportation companies, fleets, lessors, brokers, and the broader supply chain. This article breaks down what’s changing, who is most exposed, and how transportation businesses can prepare.

What the Tariff Covers — and What It Doesn’t (Yet)

Scope

- The announced tariff applies to imported medium- and heavy-duty trucks (Classes 3–8).

- The tariff was originally scheduled to take effect on Oct. 1 but was delayed to Nov. 1.

- Crucially, it remains unclear whether USMCA-compliant imports (i.e. trucks built in Mexico or Canada meeting local content thresholds) will be exempt.

- Also unresolved is the treatment of truck parts and components. Some commentators expect parts could be included or indirectly impacted via associated metal or materials tariffs.

Interaction With Other Tariffs

- Truck manufacturing already depends heavily on steel, aluminum, and other tariff-sensitive materials. Many parts are made of or incorporate materials under existing tariffs.

- Some industry observers caution that “stacking” of tariffs (i.e. applying multiple tariffs to a single item) may push costs even higher.

- Because of cross-border supply chains, components may pass through multiple countries before final assembly — complicating cost pass-through analysis.

Why It Matters to Transportation Companies

1. Higher Acquisition Cost for Trucks

If you purchase imported trucks or rely on import channels, expect tariff-driven price inflation. Some estimates suggest that a 25% import tariff combined with a 12% federal excise tax (FET) could raise the cost of a Class 8 tractor significantly — from around $170,000 to as much as $200,000+ or even $224,000 in some scenarios.

That level of cost escalation could delay or reduce new-vehicle purchases, force longer holding of older equipment, or shift demand to domestic OEMs.

2. Shifts in OEM Competitive Landscape

Companies with strong U.S. manufacturing footprints (e.g., Freightliner, Peterbilt, Kenworth, Mack) could benefit from reduced import competition.

However, parts and components cost pressures still apply even to U.S.-built units, and supply chain disruptions may ripple into pricing and lead times.

3. Impact on Fleet Renewal Cycles & Used Truck Market

With new trucks getting more expensive, many fleets may extend equipment cycles or turn toward the used truck market. That could increase competition and demand (and pricing) in the used segment.

4. Operating Cost Pressures

Even if your fleet does not directly import trucks, cost inflation may arise through:

- Replacement parts (if imported or made with tariff-impacted inputs)

- Delays or shortages in parts, increasing downtime

- Upstream supplier renegotiations or passing through additional material costs

Fleets may need to increase parts inventory buffers or reconsider sourcing strategies.

5. Rate Pressure and Revenue Pass-Through Dilemmas

Transportation companies operate in a highly competitive, low-margin environment. Many carriers will find it difficult to pass on increased capital or operating costs fully to shippers.

Some may attempt fuel or equipment surcharges or renegotiate contracts, but success will vary depending on segments (e.g. contract vs spot).

6. Strategic & Logistical Impacts

- Carriers may rush orders before Nov. 1 to avoid tariffs, accelerating shipments and putting strain on production capacity in the short run.

- Supply chain bottlenecks (ports, customs, inland transport) may get worse as shippers pull forward demand.

- Firms might reexamine cross-border sourcing, localization strategies, or vehicle sourcing from exempt jurisdictions.

Who Is Most Exposed

- Smaller fleets & independents that lack negotiating leverage or diversified sourcing channels

- Import-reliant fleets that historically imported trucks or relied on cross-border purchases

- Leasing firms and used-truck wholesalers exposed to acquisition price volatility

- Brokers and 3PLs that manage fleets or equipment leasing

- Maintenance-heavy operations (e.g. regional/dedicated fleets) reliant on imported parts

Key Questions Every Transportation Executive Should Ask

- Are any of your fleets or upcoming purchases slated to be imported trucks or sourced via foreign manufacturers?

If yes, quantify exposure (number of units, expected price delta). - Do your trucks/components meet USMCA/local content thresholds?

If exemptions apply, ensure compliance documentation is robust. - Can you accelerate orders to beat the Nov. 1 cutoff?

But be cautious not to over-order and risk excess inventory. - Can you negotiate with OEMs or brokers to share tariff burdens?

Consider cost-sharing, incremental payments, or delayed delivery windows. - Should you increase parts inventories or diversify suppliers?

Identify critical components vulnerable to tariffs or supply chain disruption. - Can you pass through costs via surcharges or rate adjustments?

Evaluate contract flexibility and customer tolerance in your markets. - Is it time to reassess fleet renewal timing?

Analyze ROI under new tariffs — perhaps hold older equipment a little longer. - Are there legal or regulatory challenges under consideration?

Some trade groups may contest the tariff’s legality (especially vis-à-vis USMCA).

Tactical Moves to Mitigate Tariff Impact

Below are steps transportation companies can take now to adapt:

A. Portfolio & Purchase Strategy

- Frontload orders where possible (without creating capacity or cash flow issues)

- Shift to domestic OEMs (if price and performance align)

- Revisit trade agreements — be sure you maintain documentation proving USMCA compliance if claiming exemption

- Lease rather than buy — may reduce exposure if leases cover depreciation rather than full capital cost

B. Supply Chain Strategy

- Audit parts and material sourcing to identify high-risk imported components

- Broaden supplier base to include more domestic sources or near-shoring

- Stock-up selectively on long-lead or critical parts before tariffs bite

- Negotiate flexibility with suppliers to share cost burdens

C. Financial Planning & Cost Control

- Model “tariff-on” cost scenarios to stress-test budgets

- Raise capital lines or liquidity now in case of cash flow pinch

- Use hedging or price escalators in procurement contracts

- Tighten maintenance scheduling to reduce wear, defer noncritical work

D. Pricing & Contract Management

- Introduce or revise equipment surcharges for new or renewal contracts

- Incorporate tariff-adjustment clauses in customer contracts where feasible

- Segment customers by cost sensitivity and ability to absorb increases

- Negotiate shared increments in long-term agreements

E. Communication & Stakeholder Engagement

- Inform customers/shippers early about expected cost impacts

- Collaborate with industry groups (e.g. ATA) to influence policy or seek clarifications

- Monitor litigation or rulemaking that may affect tariff enforcement

Potential Risks & Unknowns

- USMCA exemptions: The administration may allow exemptions for qualifying trucks built in Mexico/Canada. Whether those exceptions hold or are overridden is uncertain.

- Part-level exemptions or carve-outs: Some parts or components may be exempt or treated differently, especially if classified under separate HTS codes.

- Duration of tariff regime: It’s not yet clear how long these tariffs will remain in force — months? years?

- Legal challenges: Trade groups or trading partners may challenge the tariff’s compliance with trade treaties or domestic law.

- Macroeconomic feedback: Higher costs could reduce demand for freight, further pressuring rates and utilization.

Conclusion

The Nov. 1, 2025 tariff on imported medium- and heavy-duty trucks marks a significant shift in U.S. industrial and trade policy, with potentially profound implications for the transportation sector. While designed to protect domestic manufacturers, these tariffs will ripple across the supply chain, affecting acquisition costs, parts pricing, fleet renewal strategies, and competitive dynamics.

For transportation companies, the window is now to stress-test assumptions, renegotiate supply contracts, accelerate or delay orders strategically, and clearly communicate with customers. Those who plan proactively may be able to soften the blow — while those who wait until the tariff hits could find their margins squeezed severely.

Share with Us: