The Hidden Tax Cost of Trucking: The 15¢ Per Mile Nobody Talks About

Share this Article:

Most people think the biggest cost in trucking is fuel.

Others say it’s drivers.

Some point to insurance, equipment payments, or maintenance.

But one of the largest costs in trucking is rarely discussed at all.

Taxes.

Not income taxes. Not payroll taxes.

Transportation taxes.

And when you add them together, they can quietly add about 15 cents to every mile a truck drives.

For a truck running 100,000 miles a year, that’s $15,000 annually in taxes and regulatory fees.

For a fleet of 500 trucks, that’s $7.5 million per year.

Yet most people — including many policymakers — have little understanding of how these taxes actually work.

Let’s break it down.

The Most Taxed Vehicle on the Road

A heavy-duty truck operating in interstate commerce sits inside one of the most complex tax systems in North America.

Carriers don’t just pay one transportation tax.

They pay many of them simultaneously.

Depending on where and how a truck operates, taxes may be tied to:

• Fuel consumption

• Miles traveled

• Vehicle weight

• State registrations

• Toll road usage

• Interstate operations

Each tax exists for a reason.

Most fund transportation infrastructure like highways and bridges.

But when layered together, they create a system that most people outside trucking never see.

Start With Diesel Fuel Taxes

The largest trucking tax is hidden in plain sight: diesel fuel taxes.

Every gallon of diesel purchased in the United States includes both federal and state taxes.

The federal diesel tax is:

24.3 cents per gallon

States then add their own fuel taxes, which vary widely.

Across the country, state diesel taxes typically range from 20 cents to more than 70 cents per gallon.

When federal and state taxes are combined, diesel fuel taxes often total 55–65 cents per gallon.

Now consider the math.

A typical Class 8 truck averages roughly 6.5 miles per gallon.

If taxes total 60 cents per gallon:

That’s roughly 9 cents in tax for every mile the truck drives.

Just from fuel.

More than half of the total tax burden is literally burned through the engine one mile at a time.

Then Comes Interstate Fuel Reporting

Once a truck crosses state lines, fuel taxes become more complicated.

A truck may purchase fuel in one state but drive thousands of miles in others.

Every state expects to receive its share of the tax revenue.

To manage this, interstate carriers operate under something called the International Fuel Tax Agreement (IFTA).

Under IFTA, fleets must track:

• Every mile driven in every state

• Every gallon of fuel purchased

• Total fuel consumption

Carriers then file quarterly fuel tax reports showing how much tax each jurisdiction is owed.

IFTA simplified a previously chaotic system — but it also created a compliance machine.

Fleets must invest in:

• Mileage tracking systems

• Electronic logging devices

• Accounting software

• Administrative staff

• Audit documentation

The cost of managing this reporting infrastructure adds another 1–2 cents per mile to operations.

Taxes are not just paid with money.

They’re paid with time, technology, and administrative complexity.

The Heavy Vehicle Use Tax

Heavy trucks also pay a federal tax simply for operating on public highways.

It’s called the Heavy Vehicle Use Tax (HVUT).

Any truck weighing 55,000 pounds or more must pay this tax annually.

For most trucks, the amount is $550 per year per vehicle.

That may not sound like much compared to fuel taxes.

But spread across 100,000 miles per year, it still adds roughly:

Half a cent per mile.

Even small taxes matter when every mile counts.

Interstate Registration Fees

Next comes vehicle registration.

Most vehicles register in a single state.

Trucks are different.

Because they operate across multiple states, interstate carriers must register under the International Registration Plan (IRP).

IRP spreads registration fees across states based on where trucks actually drive.

Instead of registering in one place, carriers essentially register everywhere they operate.

Annual IRP registration fees for heavy trucks commonly range between:

$1,500 and $3,000 per truck.

Spread across annual mileage, that adds another 2–3 cents per mile.

Now Add Tolls

In some parts of the country, tolls are a major operational expense.

Major trucking corridors like:

• The Pennsylvania Turnpike

• The New York Thruway

• The Ohio Turnpike

• The New Jersey Turnpike

charge significantly higher toll rates for heavy trucks.

In many cases, a truck crossing one of these corridors can pay over $100 in tolls for a single trip.

Across national operations, tolls often add 1–2 cents per mile.

For fleets operating heavily in toll states, it can be even more.

Weight-Distance Taxes

Some states go a step further.

Instead of taxing fuel or registration, they tax trucks directly based on miles traveled and vehicle weight.

States like:

• Oregon

• Kentucky

• New Mexico

• New York

operate weight-distance tax systems.

These taxes exist because heavy vehicles create more wear on road infrastructure.

Depending on routes, these taxes can add another 1–3 cents per mile.

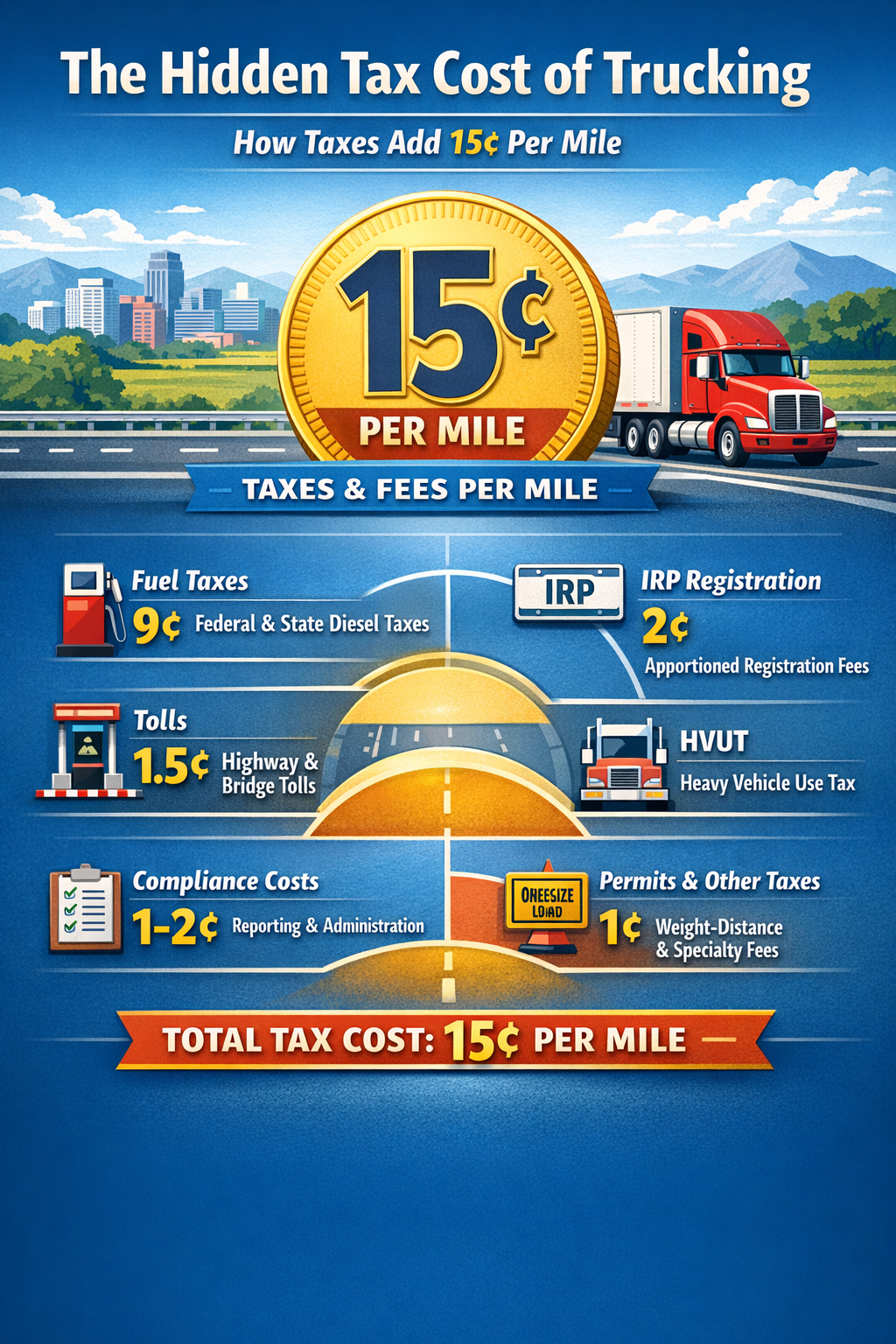

The 15¢ Per Mile Reality

When you combine all of these layers, the total tax burden becomes clear.

A typical breakdown might look like this:

Fuel taxes: ~9¢ per mile

IRP registration: ~2¢ per mile

Tolls: ~1.5¢ per mile

HVUT: ~0.5¢ per mile

Compliance costs: ~1–2¢ per mile

Weight-distance taxes and permits: ~1¢ per mile

Total:

Approximately 15 cents per mile.

Again, that’s $15,000 per truck per year for a vehicle running 100,000 miles.

For large fleets, taxes quickly become one of the largest operating costs in the business.

Why This Matters to the Economy

Trucking moves roughly 70% of domestic freight in the United States.

That means nearly everything we buy — food, clothing, electronics, construction materials — travels by truck at some point.

Transportation taxes therefore don’t just affect trucking companies.

They influence the entire supply chain.

Every additional cost in trucking eventually appears somewhere else:

• Higher freight rates

• Increased shipping costs

• Higher prices for goods

In other words:

Transportation taxes quietly contribute to inflation across the economy.

The Thin Margin Problem

One reason these taxes matter so much is because trucking operates on very thin margins.

Typical net profit margins for trucking companies are often:

3–6%.

When margins are that tight, even small cost changes matter.

Carriers usually cannot absorb major tax increases.

Instead, the costs eventually flow through to:

• Freight contracts

• Fuel surcharges

• Accessorial fees

• Spot market pricing

Taxes don’t disappear.

They simply move through the system.

Why Most People Don’t See These Costs

One reason trucking taxes remain invisible is that they’re fragmented across dozens of systems.

There’s no single “trucking tax.”

Instead there are:

• Fuel taxes

• Interstate fuel reporting

• Highway use taxes

• Registration fees

• Tolls

• Weight-distance taxes

• Permits

• Compliance requirements

Each one seems small.

Together, they create a massive cost structure.

The Policy Debate Is Just Beginning

Transportation funding is already becoming a major policy issue.

Fuel taxes historically funded most highway infrastructure.

But as vehicles become more fuel efficient — and electric vehicles become more common — governments are beginning to question whether fuel taxes will remain viable long term.

Some policymakers are exploring alternatives like mileage-based road user fees.

For trucking companies, that could mean an entirely new generation of transportation taxes in the future.

Why Understanding Trucking Taxes Matters

If you want to understand the economics of freight, you have to understand taxes.

They influence:

• Fleet operating costs

• Freight rates

• Supply chain pricing

• Infrastructure funding

• Transportation policy

For trucking companies, tax management is no longer just an accounting exercise.

It’s a strategic discipline.

One Final Thought

Next time you see a semi-truck traveling down the highway, consider what’s happening behind the scenes.

Every mile that truck travels includes:

Fuel taxes.

Highway taxes.

Registration fees.

Compliance costs.

Tolls.

Infrastructure funding.

By the time that truck reaches its destination, roughly 15 cents of every mile traveled has gone to taxes and regulatory fees.

It’s one of the most important — and least understood — cost structures in the entire transportation economy.

And it’s hiding in plain sight.

Share with Us: