Our Resources

A restructuring project lives or dies on a single question: does the new structure actually lower your tax — in every state you touch — without creating new exposure somewhere else? Answering that takes two things most firms don't pair together: deep transportation tax expertise and a disciplined project method. Transportation Tax Consulting brings both. We build the project around your footprint, not a template We start by mapping how your business is taxed today — federally and across all 51 jurisdictions where your equipment, mileage, and people create obligations. That diagnostic is where the real opportunities surface, and it's the step generalist firms skip when they reach for an off-the-shelf structure that wasn't designed for a motor carrier. We pull the levers that are specific to transportation The savings in a transportation restructure come from levers other advisors don't see: separating operating, asset-holding, and equipment-leasing entities; situating them where they reduce sales and use tax, property tax, and income and franchise tax; structuring intercompany leasing; and accounting for mileage-based apportionment, rolling stock exemptions, nexus, and the interplay of FET, IFTA, and IRP. We design the structure around how transportation is actually taxed, not how a typical business is. We model the savings before you spend a dollar restructuring Before you commit to anything, we quantify the projected effective-rate reduction and stress-test it against alternative structures. You see the numbers — state by state, scenario by scenario — including any new apportionment or nexus exposure a given option would create. The decision to proceed is driven by a model, not a hunch, and you know what the project is worth before you fund it. We quarterback execution alongside your counsel We lead the tax design and run the project end to end. The legal mechanics — forming entities and drafting agreements — sit with your attorneys, and we work in lockstep with them so the executed structure delivers the tax result it was engineered to produce. You get a single team driving the engagement, not a pile of disconnected advice. We make the result defensible and audit-ready Minimizing tax only matters if the position holds up. Every element of the structure is supported by primary-source analysis and contemporaneous documentation, built to withstand state examination and to answer, clearly, how and why the structure was put in place. We stay with you after close A structure is only as good as the compliance that follows it. We carry the project through to ongoing multistate filing and monitoring — and because we're already inside your tax data, we continue surfacing recovery opportunities and structural refinements long after the restructure is complete. The result: a measurably lower multistate tax burden, delivered by a structure that was diagnosed, modeled, executed, and defended by a team that does nothing but transportation tax.

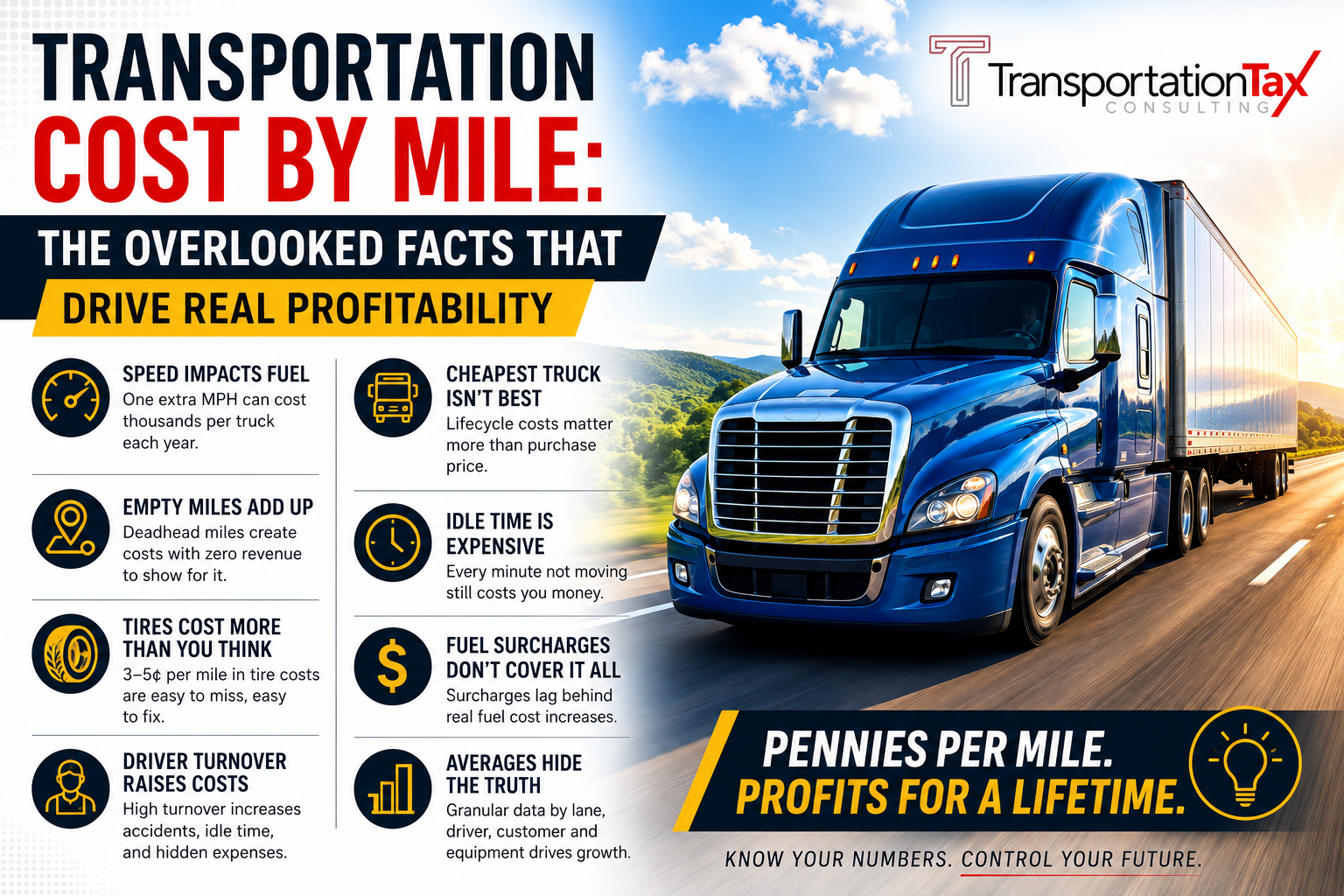

In trucking, everyone talks about rates per mile. But surprisingly few transportation professionals truly understand the hidden forces shaping those numbers. Cost per mile (CPM) is more than a spreadsheet formula — it’s the heartbeat of profitability, fleet survival, driver retention, and long-term strategy. The most successful transportation companies are not always the ones hauling the most freight. Often, they are simply the ones that understand their cost structure better than everyone else. Here are some of the most overlooked — and surprisingly fascinating — facts about transportation cost per mile. 1. One Extra MPH Can Cost Thousands Per Truck Per Year Most drivers and managers underestimate how dramatically speed impacts fuel economy. A truck running 70 MPH instead of 65 MPH may only arrive minutes earlier, but fuel efficiency can drop by 0.5 to 1 MPG depending on terrain and equipment. For a truck running 120,000 miles annually: A 1 MPG loss can increase fuel cost by over $8,000 annually per truck Across a 100-truck fleet, that can exceed $800,000 yearly The shocking part? Many fleets focus harder on rate negotiation than speed management, even though speed discipline can create larger margin improvements. 2. Empty Miles Hurt More Than Most Fleets Realize Deadhead miles are often treated as “part of trucking,” but many strategic planners fail to measure their true impact. An empty mile still creates: Fuel expense Tire wear Maintenance Driver wages Depreciation Insurance exposure A truck with a $2.00 loaded CPM may actually require $2.45+ revenue CPM when deadhead is included. The industry’s biggest hidden leak is not fuel. It’s unproductive miles. 3. Tires Cost More Per Mile Than Many Office Departments A typical long-haul tractor-trailer can burn through: 18 tires Multiple replacements yearly Thousands in alignment and wear-related issues Tires alone often account for: 3–5 cents per mile That sounds small until you realize: 5 cents × 120,000 miles = $6,000 annually per truck Poor inflation management can reduce tire life by 20% or more. Many fleets obsess over diesel prices while ignoring one of their most controllable expenses sitting literally on the ground. 4. Driver Turnover Quietly Raises Cost Per Mile Everywhere Most people think turnover only affects recruiting costs. In reality, turnover raises: Accident frequency Idle time Fuel usage Maintenance issues Insurance claims Late deliveries Customer churn A new driver often operates less efficiently than an experienced one familiar with routes, customers, and company procedures. Some analysts estimate high-turnover fleets unknowingly add: 10–20 cents per mile in indirect operational costs That can erase profitability faster than a soft freight market. 5. The Cheapest Truck Is Not Always the Most Profitable Truck Many fleets buy equipment based on purchase price instead of lifecycle CPM. A cheaper truck may: Break down more frequently Lose fuel efficiency sooner Create higher downtime costs Have lower resale value An expensive truck with better fuel economy and uptime may actually produce a lower total CPM over five years. Strategic fleets calculate: Total operating cost Residual value Maintenance curves Downtime probability Not just monthly payments. 6. Idle Time Is One of the Industry’s Most Expensive Invisible Costs A truck parked at a dock still burns money. Even when wheels are not turning: Insurance continues Driver hours are consumed Equipment depreciates Financing accrues Opportunity cost increases Some studies estimate detention-related inefficiencies can cost fleets: Tens of thousands annually per truck The most profitable fleets are often not the fastest fleets — they are the fleets with the least wasted time. 7. Fuel Surcharges Rarely Cover Actual Fuel Costs Perfectly Many shippers assume fuel surcharges completely offset fuel volatility. They usually do not. Why? Because surcharge formulas often: Lag market changes Ignore idle fuel burn Exclude reefer fuel Fail to account for out-of-route miles Use outdated baseline assumptions When diesel spikes quickly, carriers often absorb major temporary losses before surcharge programs catch up. 8. Maintenance Costs Rise Exponentially — Not Gradually A common misconception is that maintenance increases steadily over time. In reality, maintenance costs often rise like a curve. After certain mileage thresholds: Repairs become more frequent Downtime accelerates Parts failures multiply That is why some fleets trade equipment aggressively while others run equipment longer based on maintenance analytics. The smartest fleets know exactly when each truck stops being profitable. 9. Cost Per Mile Changes by Freight Type More Than Most Think Two trucks may drive identical routes but produce completely different CPMs depending on freight. Examples: Refrigerated freight increases fuel burn Heavy haul accelerates tire wear Hazmat increases insurance exposure Multi-stop freight destroys productivity Urban deliveries increase braking and idle time Many transportation professionals benchmark CPM too broadly without segmenting operations correctly. 10. The Most Dangerous Number in Trucking Is “Average CPM” Average CPM hides operational truth. One lane may be highly profitable while another silently destroys margins. One driver may average: 7.8 MPG Another: 5.9 MPG One customer may create: 30-minute turns Another: 4-hour detention delays Averages conceal inefficiency. Elite transportation strategists analyze CPM: By lane By customer By driver By trailer type By terminal By season That level of visibility separates surviving fleets from elite fleets. Final Thought Transportation cost per mile is not just an accounting metric. It is a strategic intelligence system. The fleets that dominate the future of transportation will not simply move more freight — they will understand their cost structure with greater precision than their competitors. In trucking, pennies per mile decide: profitability, expansion, acquisitions, bankruptcies, and survival. And most of those pennies are hiding in places the industry still overlooks.

Understand economic vs physical nexus, how each triggers sales tax obligations, and strategies transportation companies can use to manage multi-state compliance.

For many manufacturers, transportation is viewed as a necessary cost center—an operational function that ensures raw materials arrive on time and finished goods reach customers efficiently. Private fleets are often built to support this mission: dedicated trucks, branded trailers, and drivers aligned with company service standards. The mindset is clear—we are a manufacturer, not a trucking company. But that distinction, while operationally convenient, may be financially limiting. In today’s freight environment—marked by volatility, tightening margins, and increased competition—manufacturers operating private fleets are sitting on an underutilized asset. The question is no longer whether transportation is a cost center, but whether it could be a strategic revenue generator . By choosing not to operate as a for-hire motor carrier, manufacturers may be missing significant opportunities across revenue, cost optimization, tax strategy, and market positioning. Let’s explore what those lost opportunities look like. 1. Revenue Left on the Road The most obvious missed opportunity is direct freight revenue . Private fleets are often underutilized in one or more ways: Empty backhauls Partial loads Idle equipment during off-peak periods Regional imbalances (e.g., strong outbound lanes but weak inbound demand) A for-hire carrier monetizes all of these inefficiencies. A private carrier absorbs them. If your trucks are returning empty 30–40% of the time, that is not just inefficiency—it’s forgone revenue. In a for-hire model, those empty miles could be converted into: Spot market loads Contract freight with complementary shippers Dedicated lanes for third-party customers Even modest utilization improvements can materially change the economics of a fleet. For example, capturing revenue on backhauls alone can offset a significant portion of total fleet operating costs. Bottom line: Private carriers pay for capacity. For-hire carriers sell it. 2. Cost Structure Distortion Private fleets often operate under a different financial lens than for-hire carriers. Costs are embedded within the broader manufacturing P&L, making it harder to: Benchmark transportation performance Identify inefficiencies Optimize pricing per mile or per load Because the fleet is not generating revenue, it is judged primarily on service—not profitability. This leads to several distortions: Over-servicing certain customers without understanding true cost-to-serve Running suboptimal routes to meet internal expectations Lack of pricing discipline compared to market carriers A for-hire structure forces discipline. Every mile has a rate. Every lane has a margin. Without that framework, manufacturers may be: Subsidizing inefficient routes Masking transportation losses within product margins Missing opportunities to rationalize their network 3. Tax Optimization Opportunities One of the most overlooked differences between private and for-hire fleets lies in tax treatment —particularly in areas like fuel tax recovery, apportionment strategies, and indirect tax optimization. For-hire carriers often benefit from: More aggressive fuel tax credit optimization (e.g., IFTA positioning strategies) Better alignment of miles driven with tax jurisdictions Strategic use of leasing structures and equipment ownership models Greater awareness of exemptions and recoverable taxes tied to transportation services Private carriers, by contrast, frequently: Leave fuel tax refunds unclaimed or under-optimized Fail to align operations with tax-efficient routing Miss opportunities to structure transportation activities in a more tax-advantaged way Additionally, operating as a for-hire carrier may open the door to: Different depreciation strategies Sales and use tax advantages in certain jurisdictions Structuring transportation as a separate profit center with distinct tax planning For companies already investing heavily in fleet infrastructure, these missed tax opportunities can compound quickly. 4. Underutilized Data and Pricing Intelligence For-hire carriers live and die by data: Lane pricing Market rates Seasonal demand fluctuations Network optimization Private fleets often have this data—but don’t use it the same way. Why? Because they are not actively participating in the freight market. This creates a blind spot: You may be operating lanes that are highly profitable in the open market—but you never monetize them You may be overpaying for outsourced freight without realizing your own fleet could service it more efficiently You lack real-time pricing benchmarks to evaluate internal decisions By not engaging as a for-hire carrier, manufacturers miss the opportunity to: Develop internal pricing expertise Leverage market rate intelligence Build a more dynamic, responsive transportation strategy 5. Missed Strategic Partnerships Operating as a for-hire carrier naturally leads to relationships : Brokers Shippers Logistics providers Freight platforms These relationships create optionality. Private carriers, however, are largely inward-facing. Their networks are designed around internal needs, not external demand. As a result, they miss opportunities to: Partner with complementary shippers (e.g., filling inbound lanes) Build dedicated capacity agreements Participate in collaborative shipping models Leverage brokerage or 3PL partnerships for overflow or optimization In a tight freight market, these relationships can be invaluable—not just for revenue, but for securing capacity, managing risk, and improving service levels. 6. Asset Utilization and ROI A truck is a capital asset. So is a trailer. So is a driver. The return on those assets depends on utilization. Private fleets often struggle with: Peak vs. off-peak imbalance Seasonal demand swings Regional inefficiencies Because the fleet is designed around internal demand, it cannot easily flex to external opportunities. For-hire carriers, on the other hand: Continuously adjust to market demand Reposition assets dynamically Maximize revenue per tractor and trailer If your fleet is idle even 10–15% of the time, the ROI on those assets is compromised. The question becomes: Why invest in capacity you’re not fully leveraging? 7. Talent and Operational Expertise Operating a for-hire carrier requires a different level of operational sophistication: Dispatch optimization Pricing strategy Customer acquisition Compliance management Private fleets often have strong operational teams—but they are not always trained or incentivized to think commercially. By not entering the for-hire space, manufacturers may be: Limiting the development of transportation leadership Missing opportunities to build internal logistics expertise Falling behind competitors who are evolving into hybrid models There is also a talent attraction angle. Transportation professionals are often drawn to environments where they can: Influence revenue Optimize networks Engage with the broader freight market A purely private fleet may not offer that same appeal. 8. Competitive Disadvantage Some manufacturers are already blurring the line. Hybrid models are emerging where companies: Maintain private fleets for core operations Operate as for-hire carriers on the margin Use brokerage arms to complement physical assets These companies gain: Better cost absorption Increased revenue streams Greater flexibility in managing freight If your competitors are monetizing their fleets while you are not, they may have: Lower effective transportation costs Higher margins More resilient supply chains Over time, that gap can widen. 9. Risk Diversification Transportation markets are cyclical. So are manufacturing sectors. By operating solely as a private carrier, your transportation function is tied entirely to your core business performance. A downturn in manufacturing demand means: Less freight Lower fleet utilization Higher per-unit transportation costs A for-hire model introduces diversification: Revenue from external customers Ability to shift focus based on market conditions Greater resilience during internal slowdowns This can act as a hedge against volatility in your primary business. 10. Barriers—and Why They Exist If the opportunity is so clear, why don’t more manufacturers make the shift? There are real barriers: Regulatory requirements (FMCSA authority, compliance) Insurance complexity Operational changes (dispatch, billing, customer management) Cultural resistance (“we’re not a trucking company”) Risk of service degradation to core customers These are valid concerns. But they are not insurmountable. Many companies address them through: Creating separate legal entities for for-hire operations Starting with limited lanes or backhaul programs Partnering with brokers or 3PLs Gradually building internal capabilities The transition does not have to be all-or-nothing. 11. A Practical Starting Point For manufacturers considering this shift, the first step is not to become a full-scale carrier overnight. It’s to analyze your current network : Where are your empty miles? Which lanes have consistent volume? Where do you have geographic imbalances? What is your true cost per mile? From there, identify low-risk opportunities: Backhaul monetization Dedicated lanes with trusted partners Pilot programs in select regions Even small steps can unlock meaningful value. Conclusion: Rethinking the Role of Transportation The statement “we are a manufacturer, not a trucking company” reflects a traditional view of transportation as a support function. But in today’s environment, that view may be outdated. Transportation is not just a cost to be managed—it is an asset to be optimized. By choosing not to operate as a for-hire motor carrier, manufacturers may be leaving value on the table in the form of: Untapped revenue Inefficient cost structures Missed tax advantages Underutilized assets Limited strategic flexibility The opportunity is not necessarily to become a trucking company—but to think like one . Because the companies that do will not just move freight more efficiently. They will turn transportation into a competitive advantage.

Avoid IFTA penalties with timely, accurate filings. Learn common delay causes, best practices, and how outsourcing reduces risk and administrative burden.

When transportation companies should outsource tax preparation, plus key signs, benefits, and how it improves compliance, accuracy, and efficiency.

Understand key U.S. tax liabilities affecting maritime shipping, including sales and use tax, fuel taxes, and multistate compliance considerations.

Choose the right tax consulting partner to reduce overpayments, manage multistate compliance, and support strategic growth for transportation companies.

The transportation industry runs on thin margins, constant movement, and relentless regulatory pressure. Trucking companies focus intensely on fuel costs, driver pay, equipment expenses, insurance premiums, and freight rates. Yet one of the most overlooked forces affecting profitability often sits quietly in the background: hidden tax matters . While taxes rarely dominate daily operational conversations, they significantly influence the true cost per mile, cash flow, and long-term financial stability of transportation companies. Many carriers unknowingly overpay taxes, misapply exemptions, or overlook compliance obligations that could trigger audits and penalties. In an industry already challenged by fluctuating freight demand, rising operating costs, and tightening credit markets, hidden tax issues can quietly erode profitability. Understanding these hidden tax matters is no longer optional—it is essential. Below are several of the most common yet frequently overlooked tax issues affecting the transportation industry today. The Complexity of Fuel Tax Compliance Fuel taxes represent one of the largest tax burdens for trucking companies, yet many fleets underestimate the complexity of managing them correctly. The International Fuel Tax Agreement (IFTA) requires interstate motor carriers to track fuel purchases and miles traveled in every jurisdiction. On the surface, IFTA appears straightforward. However, the reality is far more complex. Carriers must ensure: Accurate mileage tracking by jurisdiction Proper reporting of taxable vs. non-taxable miles Correct classification of equipment Accurate fuel purchase documentation Errors in any of these areas can create major tax liabilities. Audits frequently reveal inaccurate mileage reporting or missing fuel receipts, leading to assessed taxes, penalties, and interest . Even more concerning, many companies fail to optimize fuel tax credits. When carriers purchase fuel in high-tax states but drive in lower-tax states, they may unknowingly leave money on the table by failing to properly reconcile credits. For fleets operating nationwide, these small discrepancies can add up to hundreds of thousands of dollars annually . Sales and Use Tax on Equipment Purchases Purchasing tractors, trailers, and other equipment represents one of the largest capital investments for trucking companies. Yet sales and use tax rules related to these purchases vary widely by state. Many transportation companies assume equipment purchased in one state is taxed only in that state. However, multiple jurisdictions may claim tax authority depending on: Where the equipment is titled Where it is first used Where the company has nexus Where the equipment operates For example, a tractor purchased in one state but operated in another may trigger use tax obligations in the operating state. Failure to properly address these obligations can result in significant audit exposure. Conversely, many companies miss legitimate sales tax exemptions available to motor carriers. Some states provide exemptions for rolling stock used in interstate commerce, while others offer partial exemptions or special tax treatments. Companies that fail to structure equipment purchases correctly may pay taxes that could have been legally avoided. Property Taxes on Rolling Stock Another often-overlooked tax burden involves property taxes on tractors, trailers, and other equipment . Many jurisdictions assess property tax on rolling stock based on asset value. Because equipment values can be substantial, property taxes quickly become a major operating expense. However, many transportation companies fail to properly manage this tax category. Common issues include: Incorrect asset valuations Equipment still listed after disposal Improper asset classifications Failure to claim allowable deductions Without careful review, companies may pay property taxes on equipment that has already been sold or retired. In addition, some jurisdictions allow apportionment based on miles traveled , which can significantly reduce property tax liabilities for interstate fleets. Companies that fail to take advantage of these rules often overpay. Payroll Tax and Worker Classification Risks Driver classification continues to be one of the most heavily scrutinized areas of tax compliance in transportation. Many carriers rely on independent contractors to maintain flexibility and reduce payroll costs. However, federal and state regulators increasingly challenge these classifications. If regulators determine that drivers classified as contractors should have been treated as employees, companies may face substantial liabilities, including: Payroll tax assessments Unemployment insurance contributions Workers’ compensation obligations Penalties and interest Several states have adopted stricter worker classification tests, such as the ABC test , which makes it significantly harder to classify drivers as independent contractors. Misclassification issues often emerge during audits triggered by unemployment claims or labor disputes. By the time these issues surface, liabilities may have accumulated over several years. State Income Tax and Nexus Exposure As transportation companies operate across multiple jurisdictions, determining where they owe state income tax becomes increasingly complex. Traditionally, many carriers believed they only owed income tax in the state where their headquarters was located. However, economic nexus rules and evolving tax laws have expanded state tax authority. Today, a trucking company may create tax nexus in a state simply by: Driving through the state regularly Delivering freight to customers within the state Maintaining equipment or terminals there Although Public Law 86-272 offers limited protections for certain types of interstate commerce, it does not always apply to transportation companies in the way many believe. Failure to properly address state income tax obligations can expose companies to multi-state audits and retroactive tax assessments . Tolling, Road Use Taxes, and Infrastructure Fees In addition to traditional taxes, transportation companies increasingly face non-traditional tax burdens such as tolls, highway use taxes, and infrastructure funding mechanisms. Examples include: The Heavy Vehicle Use Tax (HVUT) State highway use taxes Mileage-based road usage charges Increasing toll infrastructure Many jurisdictions view trucking companies as key contributors to infrastructure funding, and new tax structures continue to emerge. Because these taxes often operate outside traditional tax systems, they can easily escape attention during financial planning. However, when combined, they significantly impact the true cost per mile to move freight . Tax Credits and Incentives That Carriers Miss While many transportation companies worry about tax liabilities, they often overlook valuable tax credits and incentives available to the industry. Examples include: Fuel efficiency incentives Alternative fuel credits Equipment modernization credits State economic development incentives Training and workforce development credits In some cases, carriers investing in new equipment or green technologies may qualify for significant tax benefits. However, many companies never claim these credits simply because they are unaware they exist. Tax credits can directly reduce tax liability dollar-for-dollar, making them one of the most powerful financial tools available to transportation companies. Audit Exposure in the Transportation Industry The transportation industry remains a frequent audit target due to its multi-state operations and complex tax obligations. Common audit triggers include: IFTA discrepancies Sales and use tax reporting inconsistencies Payroll classification disputes Equipment purchase reporting State income tax filings Audits rarely focus on a single tax category. Instead, they often expand into multiple areas once regulators begin reviewing company records. For companies without strong tax compliance processes, audits can quickly become expensive and time-consuming. However, companies that proactively review their tax exposure often discover refund opportunities and risk reduction strategies before regulators ever arrive. The Connection Between Hidden Taxes and Cost Per Mile Every tax obligation ultimately feeds into one critical metric in the transportation industry: cost per mile . Fuel taxes, equipment taxes, payroll taxes, and infrastructure fees all contribute to the total cost required to move freight. Yet many companies underestimate the role tax strategy plays in controlling that number. When tax issues remain hidden or unmanaged, they inflate operating costs in ways that may not immediately appear on financial statements. Over time, these hidden costs can affect: Freight pricing strategies Profit margins Equipment investment decisions Cash flow management Company valuation In a competitive freight market, even small improvements in tax efficiency can significantly impact overall profitability. Why Transportation Companies Must Take a Proactive Approach The most successful transportation companies no longer treat tax compliance as a year-end accounting task. Instead, they approach it as a strategic operational function . Proactive tax management includes: Regular tax exposure reviews Multi-state tax compliance analysis Equipment purchase planning Worker classification evaluations Fuel tax optimization By identifying hidden tax issues early, companies can avoid penalties, recover overpaid taxes, and strengthen financial performance. More importantly, proactive tax planning provides leadership teams with a clearer understanding of their true operating costs . The Industry Cannot Afford to Ignore Hidden Tax Issues The transportation industry continues to face major economic pressures, including fluctuating freight demand, rising insurance costs, equipment shortages, and driver challenges. Hidden tax matters only add to that pressure. Yet these issues often remain buried within accounting systems, compliance processes, or outdated operational practices. Companies that ignore them risk: Overpaying taxes Facing unexpected audits Losing competitive advantage Reducing profitability The good news is that many of these issues are correctable once identified . Call to Action: Take Control of Your Transportation Tax Exposure Hidden tax issues rarely fix themselves. They require intentional review and proactive management. Transportation companies should regularly ask themselves: Are we overpaying fuel taxes? Are our equipment purchases structured correctly for sales tax? Are we properly managing property taxes on rolling stock? Are driver classifications defensible under current regulations? Are we exposed to multi-state tax risks? If leadership teams cannot confidently answer these questions, it may be time for a comprehensive tax review. The transportation industry already operates in a challenging economic environment. Companies cannot afford to let hidden tax matters quietly erode profitability. Now is the time to uncover those hidden tax issues, strengthen compliance, and ensure your company keeps more of the revenue it earns moving freight across America. Because in trucking, every penny per mile matters.