Sales Tax Refunds for Transportation Companies: Expert Guide 2025

Share this Article:

Introduction to Sales Tax Refunds in the Transportation Industry

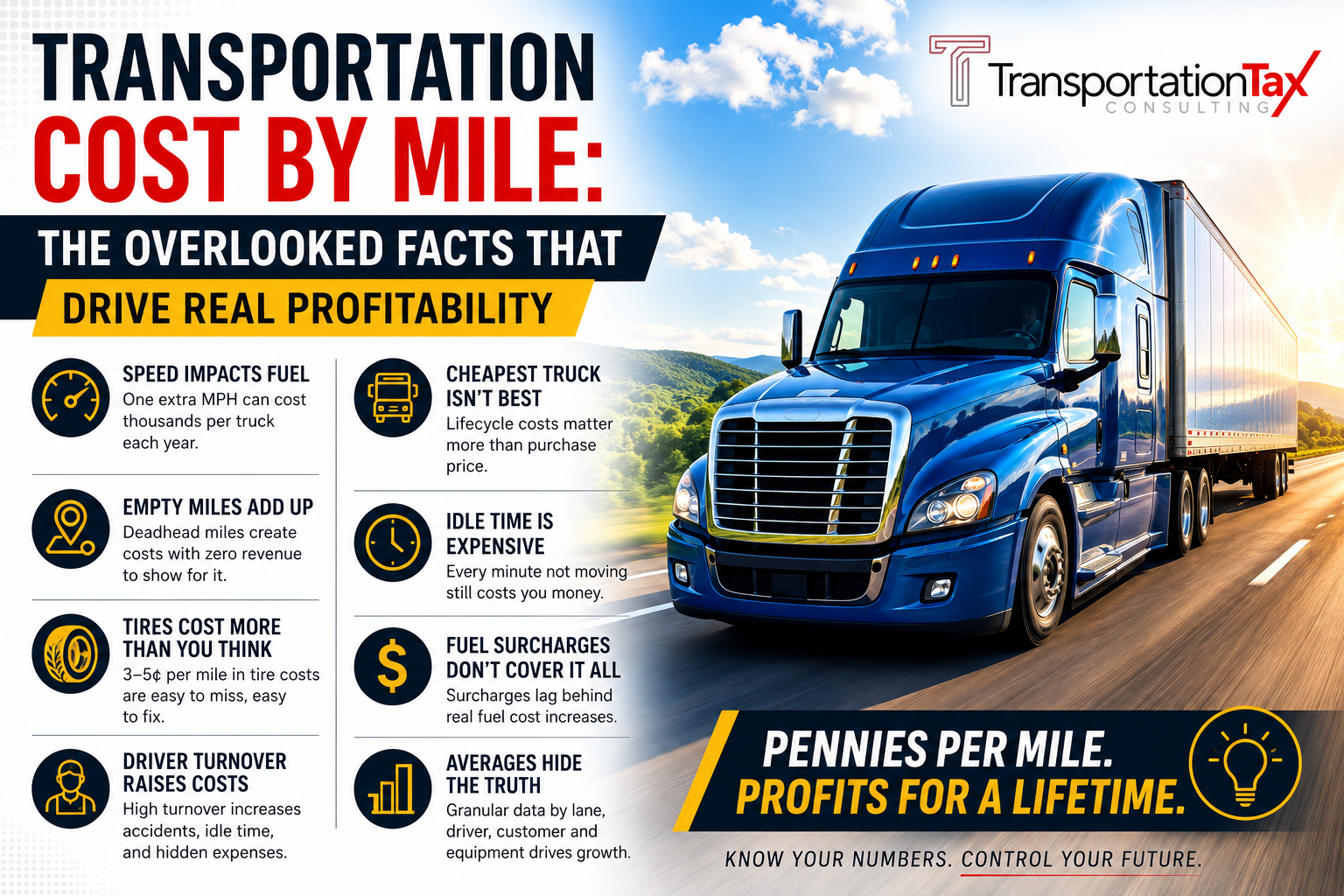

Transportation companies often operate across states and borders, making their sales tax obligations complex and prone to overpayments. However, these companies are also uniquely positioned to claim sales tax refunds—if they understand the rules. This guide demystifies the refund process, helps businesses identify refund opportunities, and outlines how to file claims effectively in 2025.

Understanding Sales Tax in Transportation Businesses

What is Sales Tax and How it Applies to Transportation

Sales tax is a consumption tax levied on goods and certain services. In transportation, the taxability varies by state and depends on the nature of the service—whether it's freight, logistics, passenger transport, or vehicle rentals.

Common Taxable and Non-Taxable Services

- Taxable: Intra-state freight, vehicle rentals, rideshare services

- Non-Taxable: Interstate shipments, exempt clients (e.g., government contracts), certain public transport

Misunderstanding these categories often leads to overpayments—prime candidates for refunds.

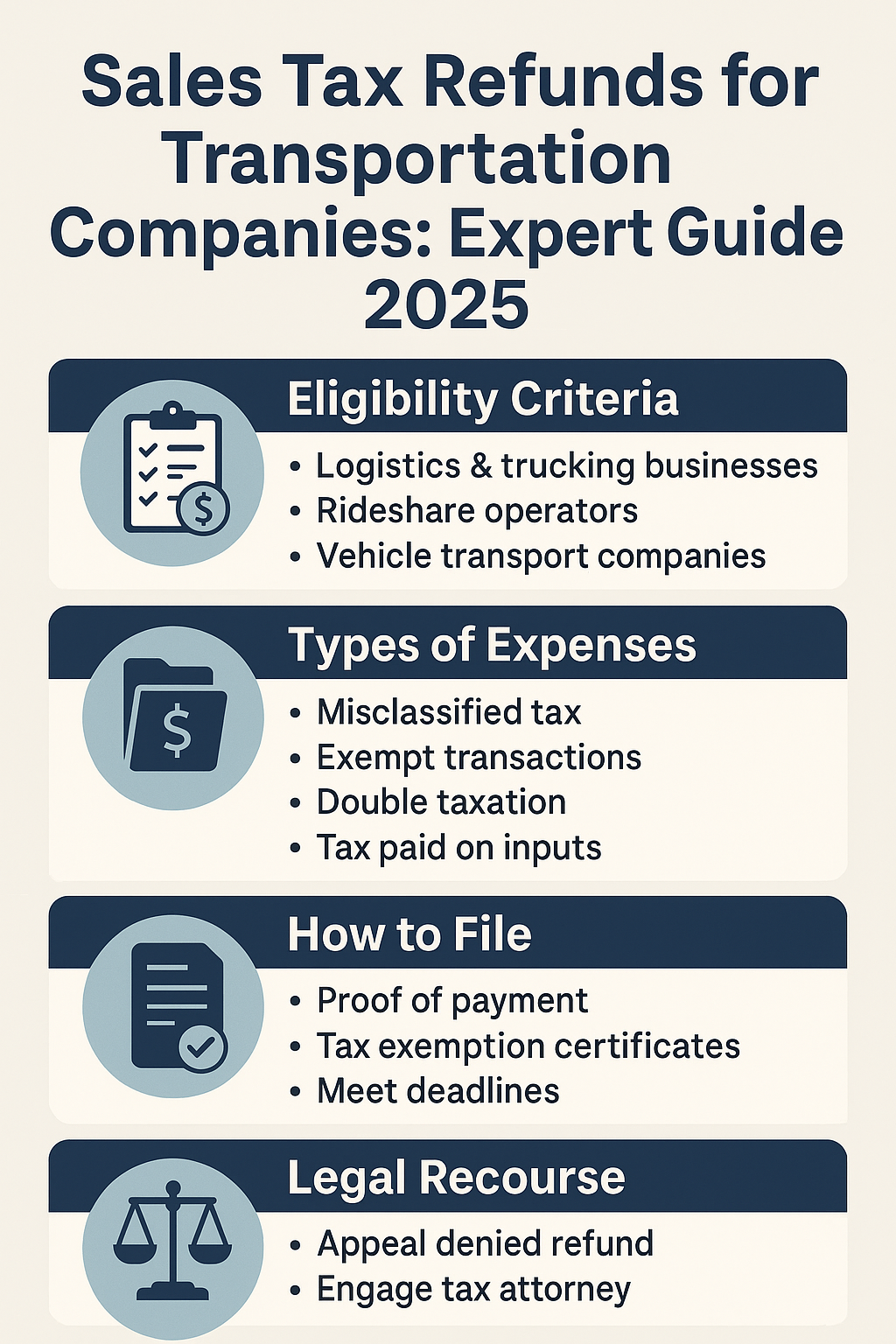

Eligibility Criteria for Sales Tax Refunds

Who Can Claim Refunds?

- Logistics companies

- Trucking businesses

- Rideshare operators

- Charter bus services

- Vehicle transport companies

Refunds can be claimed by companies directly or by third-party consultants acting on their behalf.

Types of Expenses Eligible for Refund

- Over-collected tax due to misclassification

- Tax on exempt transactions

- Double-taxed services across jurisdictions

- Sales tax paid on inputs used in tax-exempt services

Scenarios Where Refunds Apply for Transportation Companies

Out-of-State Sales and Exemptions

If a service is provided across state lines and taxed in both jurisdictions, businesses can often claim a refund from one state based on reciprocity rules.

Double Taxation or Tax Overpayments

For instance, if a company pays both use tax and sales tax on the same service or goods, it's entitled to a refund of the duplicate tax.

Tax-Exempt Clients or Contracts

If services are provided to entities like non-profits or government agencies—and taxes were charged in error—refunds are typically allowed with supporting documentation.

How to File for a Sales Tax Refund

Required Documentation and Records

- Proof of payment (invoices and receipts)

- Tax exemption certificates (if applicable)

- Shipping documents or bill of lading

- Contracts or customer agreements

Online vs. Paper Filing Methods

Most states allow online filing through their Department of Revenue portals. Paper filings are still accepted in some jurisdictions but may take longer to process.

Time Limits and Deadlines by State

Statutes of limitations vary, but the window is typically 3-4 years from the date of payment. Missing the deadline forfeits your refund rights.

State-by-State Guidelines for Refunds

States with Favorable Refund Policies

- Texas: Allows online submission and quick turnaround.

- Florida: Provides specific refund processes for logistics and trucking.

- California: Offers refunds on overstated local and district taxes.

Special Rules for Logistics and Trucking Companies

Many states offer exemptions or credits for diesel fuel used in interstate commerce. Refund claims often require International Fuel Tax Agreement (IFTA) records.

Federal Considerations and Refund Claims

IRS Guidelines Related to Transport Tax Refunds

While sales tax is state-governed, federal tax deductions may apply for sales tax paid on business purchases, particularly if the refund was denied at the state level.

Interaction Between State and Federal Refunds

Some companies mistakenly double-dip—claiming refunds at the state level and deducting the same amounts federally. This can trigger audits, so coordination is critical.

Common Mistakes in Filing Sales Tax Refunds

Incomplete Documentation

Missing proof of tax paid or shipping documentation is the #1 reason for refund denials.

Misclassification of Services

Claiming refunds for services that are taxable under state law will get denied and may prompt further scrutiny or penalties.

Best Practices for Managing Sales Tax Refunds

Keeping Accurate Transportation Logs and Invoices

Logs showing mileage, shipping destinations, and client details support refund claims—especially for interstate services.

Using Tax Software and Consultants

Platforms like Avalara or Vertex help automate tax classification and monitor overpayments. Refund consultants can help file large or complex claims.

Examples and Case Studies

Real-World Cases of Successful Refund Claims

A California-based trucking company recovered over $45,000 in sales tax paid on exempt interstate hauls by filing detailed records and proof of exemption.

Lessons Learned from Denied Refunds

A Midwest shuttle service was denied $12,000 in refunds due to incomplete contracts and missing exemption certificates—highlighting the importance of recordkeeping.

Legal Recourse if Refunds Are Denied

Appealing a Denied Refund Request

Each state offers an appeals process. Companies may file an administrative review or formal hearing with the state’s tax authority.

Working with State Departments or Legal Counsel

Engaging a tax attorney may be necessary for complex or high-value claims. Mediation services are sometimes available through the state.

FAQs About Sales Tax Refunds for Transportation Companies

1. How long does it take to receive a sales tax refund?

Usually 4–12 weeks, depending on the state and completeness of the application.

2. Can small transportation businesses apply for refunds?

Yes. Even sole proprietors or independent operators can claim refunds if eligible.

3. Are fuel taxes included in sales tax refunds?

Not usually. Fuel taxes are separate and refunded through IFTA processes.

4. What if I overpaid sales tax two years ago—can I still claim?

Yes, if your state’s statute of limitations is three years or more.

5. Should I use a third-party firm to file my refund?

If the claim is complex or involves multiple states, yes—third-party firms can improve accuracy and approval chances.

6. Can I automate future refund detection?

Yes. Tax platforms like TaxJar or Avalara offer refund detection and alerts for overpaid taxes.

Conclusion: Turning Overpaid Tax into Savings

Navigating sales tax refunds for transportation companies may seem daunting, but it’s a highly beneficial process when done correctly. From avoiding overpayments to recovering thousands in improperly collected taxes, these refunds can significantly impact your bottom line. By maintaining organized records, leveraging modern tools, and understanding your state’s tax landscape, your transportation business can unlock valuable savings and operate with greater financial confidence.

Share with Us: